Easiest Game Show To Win Money

Morning hustlers! You ready for a new week? A new chance to improve your finances? How about your mind at the same time? :)

Came across another money test on the internets, and according to The Motley Fool if you don't answer these questions right you're financially illiterate (d'oh).

Here are the 5 questions below, along with my own answers and then followed by theirs. Try to answer them first before cheating and see where you fall. Fingers crossed for you!

#1. What is your net worth?

Starting off with an easy one I see! $490,000. #BOOM I swear if you don't know this one by now I've failed you as a blogger…

#2. Is it more important to pay off high-interest rate debt or save for retirement first?

I'm going to go with "pay off debt." I can't say whether it' more important or less important as retirement since both are pretty damn important!, but I know emotionally speaking it's much more gratifying killing your debt than it is saving for something 40+ years away. Early retirement scenarios excluded. And in either event, your debt will need to be gone regardless!

I also don't know of an investment that will give you a higher rate of return than high-interest c/c debt (I'm guessing we're talking 15% and higher?) and that's also *guaranteed*. With each credit card payment you're essentially locking in your return – and a high one at that – so yeah, I'm gonna go with "paying debt down first", Alex!

#3. When should you start saving for retirement?

Dang it!! I want to say TODAY, but I just spent the past 8 seconds convincing you that your high-interest debt needs to be paid off first! Arghhh…

So I guess, after debt? But that doesn't sound right… I'd never wait until debt is gone to start saving for retirement. Especially if you get FREE MONEY from employer 401(k) matches! Which you should definitely do regardless of debt because that's an automatic 50%-100% return right off the bat depending on your company. And also guaranteed!

So my official answer here is: Start saving for retirement today, if you can take advantage of some kick-ass perks, and if not just hustle to get your crazy debt killed first while still throwing at least a few dollars towards retirement until you can put it in full throttle. I think it'll make you feel better even if it's not 100% financially "smart," and honestly any decision you make here gets you closer to freedom.

#4. How much money will you need to have accumulated for retirement?

We're getting trickier as we go :) But when you've finally commit to chasing early retirement (ie. financial freedom), one of the first things you do is run your numbers to see how far you have to go and where you're starting from. Which requires knowing how much you spend each month (or how much you *think* you'll spend in the future in retirement – as best you can), as well as your best guestimate of income needed to accomplish it. Whether from stocks, rental properties, pension checks, social security (hah!) or any other forms of passive/semi-passive income.

In other words, the amount you need to retire will be completely different than your neighbor's. And if anyone ever tells you different they don't know what they're talking about.

It all hinges on your *expenses*. The more you need to live off, the more you'll need for retirement (makes sense, right?). And to figure out how much you'll need in retirement, a quick calculation you can do is multiply your yearly expenses by 25 – a "rule" most in the E.R. community go off.

For us, this means $1,560,000 in income-producing assets in order for us to retire fully ($5,200/mo x 12 x 25). With the focus on income-producing assets. The house you live in or the $100,000 rare coin you own (you lucky bastard) doesn't count unless you're selling it.

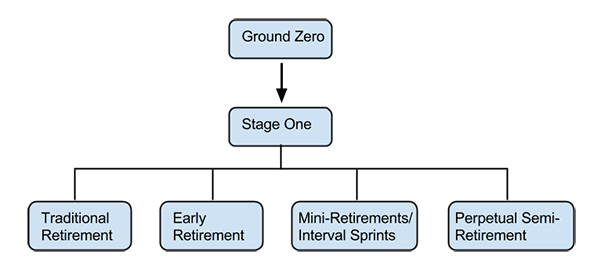

But keep in mind there are *stages* to retirement too. It doesn't have to be an "all or nothing." As my friend Paula puts it, there are mini-retirements, semi-retirements, and even retirement sprints! Where you work for a few months, and then play for a few months (yum). Feast your eyes:

I see myself in the perpetual semi-retirement phase as I'll always be working on something even though I don't need the money anymore. It's just those *somethings* are whatever the hell I want them to be ;)

I see myself in the perpetual semi-retirement phase as I'll always be working on something even though I don't need the money anymore. It's just those *somethings* are whatever the hell I want them to be ;)

If you want a fun spreadsheet to play with, plug your numbers into my early retirement calculator and see what it spits out. Knowing your date (and age) when you can retire puts everything in much clearer perspective. And can be incredibly empowering as well.

#5. Do stocks, bonds, or real estate grow fastest over long periods?

STOCKS!!!! Bonds are slooooow and don't net you much (I don't think?), and real estate, well, we all know how real estate is :) In theory it holds its value and only goes up, but as far as being "fast" I'd say depends on market and location conditions. Something I'm quite obviously not an expert in. My guess would be stocks, real estate, and then bonds.

**Answer Key**

A1. Net worth — You either know it or you don't! Add up all your assets (savings, investments, real estate), subtract your liabilities (debts, loans), and presto – your net worth.

A2. Debt or retirement? — The Fool says high-interest debt first all day, every day. Basically comparing 10% (hopeful) market returns to 25% (vomit-producing) credit card debt. Which apparently some people have?? How is that even legal?? Anyways, they say that with lower interest rate debts it's fine to manage while at the same time saving for retirement. Which is the case for us, and I imagine any other homeowner under the age of 50 since most carry mortgages for (what seems like) forever.

A3. When to save for retirement? — "As soon as possible!" Laaaaame. But also very true – which is why questions like these suck cuz you'll never get a straight answer since WE'RE ALL IN DIFFERENT STAGES. The real question to figure out is when it's "possible" for you. And, realistically, it's usually a lot sooner than you think. Which is why I say to start TODAY even if it's a measly $5.00. You won't miss it, and it'll get the ball rolling that much faster.

A4. How much money do you need for retirement? — "There's no one-size-fits-all answer here." Aww man! I wanted to not listen to them anymore ;) But it is good to see they go off the 25x yearly expenses idea too. I'm telling you, it's all about those expenses in our lives! Gotta keep challenging them to push 'em lower and lower. The less you need to live off, the less you need to make!

A5. What's quicker – stocks, bonds, real estate? – Stocks! Ding ding ding! And then according to their charts (which spanned from 1802-2012), bonds are next. Though it didn't include real estate:

- Stocks @ 8.1% (9.6% between 1926 to 2012)

- Bonds @ 5.1%

- Bills @ 4.2% (Treasury bills?)

- Gold @ 2.1%

- U.S. Dollar @ 1.4%

Full story and answers here: The Financial Literacy Test

How did you do? You make me a proud blogger?? :)

Where I stand, the most important questions here were #1 and #4. You concentrate on those and the rest will follow – no matter which route you take to improve them.

And always remember: The only reason we pay attention to money is to hopefully not need to one day! Until then, you play the game the best way you can.

******

[photo by thierry ehrmann / dollar-fied by J$]

Jay loves talking about money, collecting coins, blasting hip-hop, and hanging out with his three beautiful boys. You can check out all of his online projects at jmoney.biz. Thanks for reading the blog!

Easiest Game Show To Win Money

Source: https://www.budgetsaresexy.com/financially-literate-test/

Posted by: tillmondeggence45.blogspot.com

0 Response to "Easiest Game Show To Win Money"

Post a Comment